Location

Location

Login

Login

TL;DR:

- Golf cart financing spreads costs over time, making purchases more practical for buyers.

- Multiple financing options exist, with terms depending on credit score, cart use, and model age.

- Proper preparation and understanding loan details help avoid costly mistakes and ensure a smooth process.

Golf carts can run anywhere from $5,000 to over $15,000 depending on the model, features, and whether you’re buying new or used. For most individuals and small business owners, paying that full amount upfront simply isn’t practical. Financing gives you a way to spread that cost over time, protect your cash flow, and still get the cart you actually need. Whether you’re buying a single cart for personal use on your property or putting together a small fleet for a commercial operation, understanding your financing options, preparing the right documents, and managing your loan responsibly can make the difference between a smart purchase and a costly mistake.

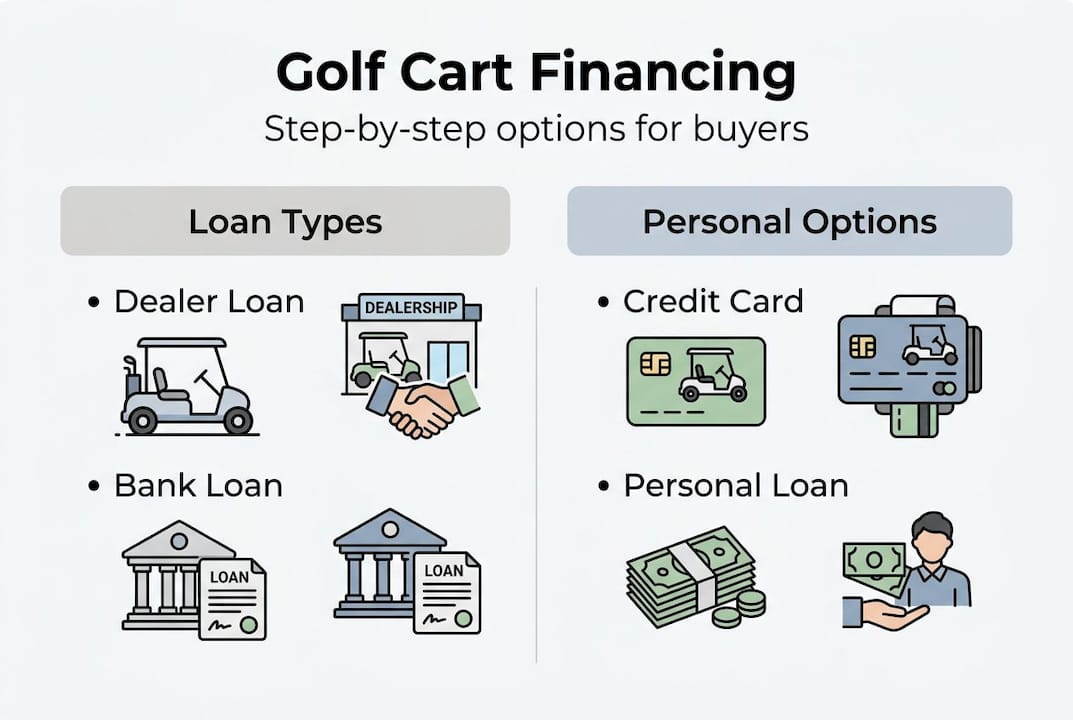

Understanding your golf cart financing options

Now that you understand why financing makes sense, let’s look at the various ways you can fund your golf cart purchase. There are several ways to finance a golf cart, each with its own trade-offs depending on your credit profile, how you plan to use the cart, and how much you want to put down upfront.

Here’s a breakdown of the most common financing methods:

| Financing type | Typical APR | Term length | Best for | Key drawback |

|---|---|---|---|---|

| Dealer financing | 0% to 14.99% | 12 to 60 months | New cart buyers | Promotional terms may have penalties |

| Bank or credit union loan | 6% to 18% | 24 to 72 months | Buyers with good credit | Requires strong credit history |

| Personal loan | 8% to 30% | 12 to 60 months | Quick approval needs | Higher rates for lower credit |

| Credit card | 18% to 29.99% | Revolving | Small balance purchases | Very high long-term cost |

| Business financing | 5% to 20% | 12 to 84 months | Commercial fleet buyers | Requires business documentation |

The right choice depends on a few key factors:

- Your credit score: Higher scores unlock lower rates and better terms across all options.

- Business vs. personal use: Commercial buyers often qualify for dedicated business loan programs with tax advantages.

- Down payment amount: A larger down payment reduces your financed balance and typically improves your rate.

- New vs. used cart: Some lenders restrict financing on older used models, especially those over 10 years old.

- Cart type and value: Whether you’re looking at electric vs gas golf carts can affect resale value and lender willingness to finance.

Dealer financing is often the most convenient starting point, especially when promotional zero-interest periods are available. However, those promotions usually require excellent credit and carry deferred interest clauses, meaning if you don’t pay off the balance in time, you could owe back interest from day one. Bank loans and credit unions tend to offer more transparent terms, while personal loans work best when you need fast approval and don’t want to go through a dealer. For business owners, dedicated commercial financing programs are worth exploring because they often allow you to deduct interest payments as a business expense. Knowing what cart works best for your area also helps you narrow down the right model before you apply.

Requirements and preparation before applying

With a clear sense of your financing options, it’s time to prepare everything needed to secure approval. Lenders assess credit history, income, and the intended use of the cart when making financing decisions, so being prepared before you apply puts you in a much stronger position.

Here’s what most lenders will ask for:

| Document | Personal buyer | Business buyer |

|---|---|---|

| Government-issued ID | Required | Required |

| Proof of income | Pay stubs or tax returns | Business tax returns or P&L |

| Credit score | 600 or above preferred | 650 or above preferred |

| Cart details | Make, model, price, VIN | Same, plus intended use |

| Business documents | Not required | EIN, business license, formation docs |

Follow these steps to prepare before submitting any application:

- Check your credit report. Pull your report from all three bureaus and dispute any errors before applying.

- Compare cart prices. Know the exact model and price so your loan amount is accurate and realistic.

- Gather your paperwork. Collect income documents, ID, and any business registration records in advance.

- Understand business tax perks. If you’re buying for commercial use, consult a tax advisor about Section 179 deductions.

- Review street legal golf cart criteria. Carts used on public roads may require additional insurance or registration, which affects lender requirements.

- Inspect used models carefully. If you’re financing a used cart, review the guide on inspecting used golf carts to avoid buying something with hidden issues.

Common mistakes buyers make at this stage include submitting incomplete applications, not disclosing the cart’s intended commercial use, and underestimating total costs like insurance and registration fees. These gaps can delay approval or result in worse terms.

Pro Tip: Increasing your down payment by even 10 to 15 percent can meaningfully lower your monthly payment and may push you into a better rate tier with some lenders. If your credit score is borderline, spending 30 to 60 days paying down existing balances before applying can make a real difference.

Step-by-step process for financing a golf cart

Now that your documentation and eligibility are in order, here’s exactly what to expect as you move through the financing process. Financing a golf cart follows an automotive loan-like process: research, apply, verify, and close. Knowing each step in advance prevents surprises and helps you negotiate from a position of confidence.

- Choose your cart. Browse models that fit your use case and budget. The energy source you choose (electric vs. gas) affects the purchase price, which directly shapes your loan amount.

- Estimate total costs. Add up the cart price, taxes, registration, insurance, and any accessories. This is your true financing target.

- Select a lender or dealer program. Decide whether you want to apply through the dealer, your bank, a credit union, or an online lender. Get pre-qualified if possible.

- Submit your application. Fill out the application completely and accurately. Attach all required documents at this stage to avoid delays.

- Review the loan offer carefully. Look at the APR, total repayment amount, term length, prepayment penalties, and any deferred interest clauses before agreeing to anything.

- Sign and receive funding. Once you sign, funds are typically released to the dealer within one to three business days. You take delivery of the cart and your repayment schedule begins.

Pro Tip: Always ask the dealer directly whether any zero-interest promotions are available and what the exact conditions are. Some promotions require automatic payments or a specific credit tier to qualify. Also ask whether the payment schedule is flexible, as some lenders allow biweekly payments that reduce your total interest paid.

Factors that affect your final rate include your credit score, the cart model and its value, the loan term you choose, and whether the cart is for personal or commercial use. Longer terms lower your monthly payment but raise the total interest you pay. After you apply, most decisions come back within 24 to 72 hours. If you’re ready to explore financed golf cart models, having your pre-qualification in hand makes the buying process much faster.

After approval: verification, payment schedules, and common mistakes

Once your financing is approved and the golf cart is in your hands, staying on top of your commitment is crucial. Before you sign anything, review the full loan contract carefully. Pay close attention to the interest rate, total repayment amount, loan length, any fees for late payments, and whether the lender requires you to carry specific insurance coverage on the cart.

Here’s what to stay on top of after your loan closes:

- Set up automatic payments. This prevents missed payments and some lenders offer a small rate discount for autopay enrollment.

- Track your payoff balance. Know where you stand at any given time, especially if you plan to sell or trade the cart before the loan ends.

- Understand early payoff rules. Some loans include prepayment penalties, meaning paying off early could cost you a fee. Confirm this before sending extra payments.

- Handle missed payments proactively. If you know you’ll miss a payment, call your lender before it happens. Many will work with you on a deferral rather than reporting a delinquency.

- Consider refinancing. If your credit improves significantly after origination, refinancing at a lower rate can reduce your remaining interest cost.

Ignoring loan obligations on a financed golf cart carries real consequences. Missing payments can result in added fees, damage to your credit score, or repossession of the cart. Don’t wait until you’re behind to reach out to your lender.

For business buyers, keeping detailed records of how the cart is used for commercial purposes supports any tax deductions you claim. If your needs change and you want to sell or transfer a financed cart, you’ll need lender approval first, since the cart serves as collateral. Knowing how to choose the best golf cart for your needs upfront reduces the chance you’ll want to swap it out mid-loan.

A fresh perspective on golf cart financing

Most financing guides focus on APR and monthly payments. That’s a starting point, but it’s not the full picture. What we’ve seen is that buyers who focus only on the monthly number often underestimate what the total cost of ownership actually looks like once you factor in insurance, maintenance, battery replacement for electric models, and any upgrades needed for commercial use.

Here’s something most guides skip: used and certified pre-owned golf carts are fully financeable and often represent a smarter buy. A two or three-year-old cart at 60 percent of the new price, financed at a modest rate, can cost you far less over three years than a new model with a flashy zero-percent promotion that carries a deferred interest trap.

Leasing also gets dismissed too quickly. For small businesses that need to rotate equipment or upgrade frequently, a lease can actually improve cash flow and keep you on newer, more reliable equipment without the depreciation risk. The key is reading every clause. Some dealer financing deals look great on the surface but include strict early termination penalties or mandatory service contracts that quietly add to your cost. Go in with your eyes open, and always run the numbers on total payout, not just the monthly figure.

Find competitive golf cart deals and financing

Ready to find your next golf cart at a great rate? Here’s where you can start browsing and applying instantly.

IMAGE:cta_image]

At Import Junkies, we carry a wide range of golf carts built for personal use and commercial operations, with financing options designed to fit different budgets and credit profiles. You can browse our [4-seater electric cart or check out our 6-seater gas model for larger groups and commercial needs. The application process is straightforward, and our team is available to answer questions about terms, eligibility, and cart selection. Browse all available carts and financing options and take the next step toward ownership today.

Frequently asked questions

Can I finance a used golf cart or only new models?

You can finance both new and used golf carts, though some lenders may set minimum or maximum age requirements for used models, so always confirm eligibility before applying.

What credit score do I need to get golf cart financing?

Most lenders look for a score of 600 or above, but credit requirements vary by lender, and some programs exist for buyers with lower scores who can provide a larger down payment.

Is leasing a golf cart a better deal than buying?

Leasing offers lower monthly payments and easier upgrades, but buying builds equity and costs less over the long term. Both options have trade-offs depending on your use case and how long you plan to keep the cart.

Can I get business financing for a fleet of golf carts?

Yes, many lenders offer dedicated programs for commercial and fleet purchases, and financing options differ significantly between individual and business buyers in terms of documentation and available terms.

What happens if I miss a payment on my financed golf cart?

Missed payments can lead to late fees, credit damage, or repossession, so contact your lender early if you anticipate any trouble making a scheduled payment.

Key Takeaways

| Point | Details |

|---|---|

| Multiple financing options | Loans, leases, dealer offers, and personal credit all work for buying golf carts. |

| Preparation is crucial | Gather documents and check your credit before you apply to qualify for better rates. |

| Understand the terms | Review contracts for hidden fees, penalties, and the total cost of ownership. |

| Business and personal buyers differ | Requirements and loan programs may change depending on your intended use. |

| Stay on top of payments | Missed payments can lead to added costs or loss of your golf cart, so track your schedule closely. |

Recommended

- How to inspect used golf carts: a step-by-step guide – Saferwholesale || Import Junkies || Great Sports

- Customize your golf cart: complete personalization guide – Saferwholesale || Import Junkies || Great Sports

- Best Golf Cart for Neighborhoods: What to Buy – Saferwholesale || Import Junkies || Great Sports

- Street Legal Golf Cart Requirements Explained – Saferwholesale || Import Junkies || Great Sports

- Top golf cart modifications to boost style and performance — GOLFCARTSTUFF.COM™