Location

Location

Login

Login

TL;DR:

- Financing an RV involves understanding credit profiles, loan options, and lender rates to avoid overspending. Most lenders require a minimum credit score of 680, with better rates available for scores above 740, and down payments of at least 20% improve terms. Comparing offers from multiple lenders and budgeting for total ownership costs helps ensure affordable, responsible RV ownership.

Financing a recreational vehicle, commonly called an RV loan in the lending industry, is achievable when you understand your credit profile, loan term options, and which lenders offer the most competitive rates. Banks, credit unions, specialty RV lenders, and dealership financing all serve this market differently, and choosing the wrong one can cost you thousands over the life of the loan. This guide walks you through every step of how to finance recreational vehicles, from checking your credit score to closing the deal, so you can get on the road without overpaying.

What loan options are available for financing recreational vehicles?

RV financing is a secured loan product, meaning the vehicle itself serves as collateral. That distinction matters because lenders set strict eligibility rules around the vehicle’s age, condition, and value.

The four main sources for recreational vehicle loans are:

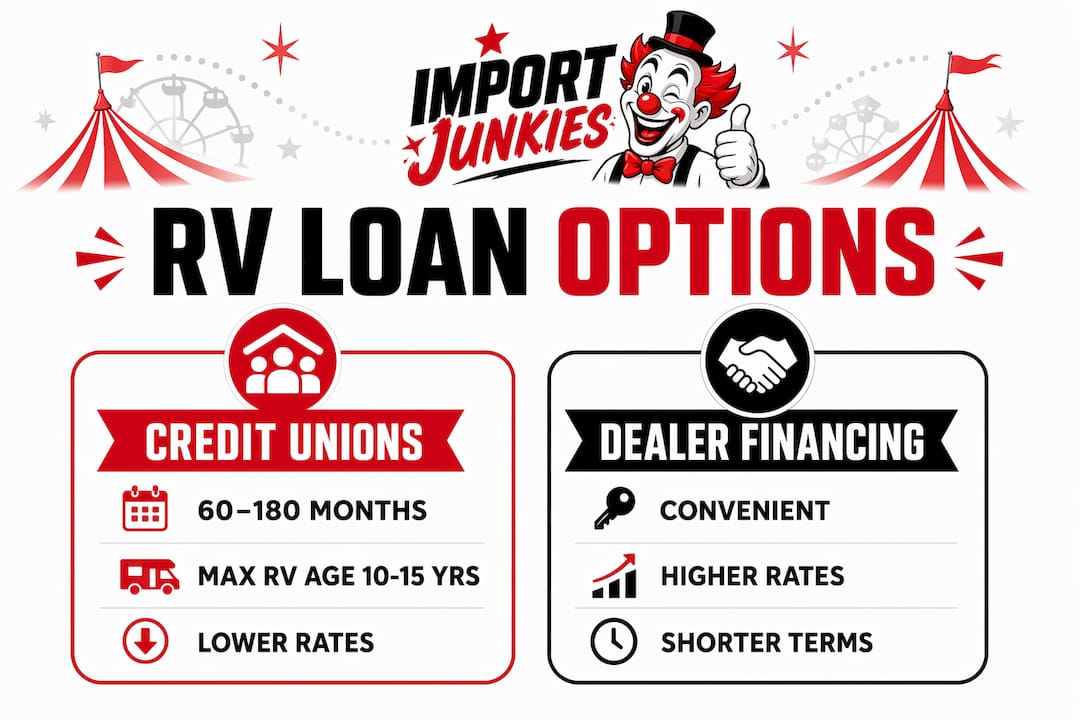

- Banks and credit unions: Credit unions like Navy Federal Credit Union often offer lower rates and more flexible terms than commercial banks. They prioritize member relationships over profit margins.

- Specialty RV lenders: These lenders focus exclusively on recreational vehicle loans and understand the market better than general auto lenders.

- Online lenders: Platforms like LendingTree connect you with multiple lenders at once, letting you compare offers quickly.

- Dealership financing: Convenient but often the most expensive option, as dealers earn a commission on the rate they sell you.

RV loan terms typically range from 60 to 240 months, or 5 to 20 years, depending on the loan amount and lender. Longer terms lower your monthly payment but increase total interest paid. Shorter terms cost more per month but save money overall.

One critical restriction to know: lenders often cap financing for RVs that are 10–15 years old to reduce collateral risk from depreciation. If you are buying a used RV older than that threshold, you may need a specialty lender or a personal loan instead.

| Lender Type | Typical Loan Terms | Max RV Age | Rate Range |

|---|---|---|---|

| Credit Unions | 60–180 months | Up to 15 years | Competitive, member-based |

| Banks | 60–240 months | Up to 10–12 years | Varies by credit tier |

| Specialty RV Lenders | 120–240 months | Up to 15 years | Mid-range |

| Dealership Financing | 60–180 months | Varies | Often highest due to markup |

Knowing which lender fits your situation before you walk into a dealership gives you real negotiating power.

How do credit score and down payment affect your RV loan?

Your credit score is the single biggest factor lenders use to set your interest rate. Lenders require a credit score of at least 680 for competitive rates, and borrowers with 740 or above qualify for the best available APRs. That gap matters more than most buyers realize.

Typical RV loan interest rates for good credit fall in the 6–8% range. Borrowers with near-prime scores pay noticeably higher rates and may face larger required down payments. On a $40,000 loan over 10 years, even a 1.5% rate difference adds up to thousands of dollars in extra interest.

Your down payment size also shapes your financing terms directly:

- A 20% or larger down payment lowers your interest rate by 0.5–1.0% and protects you from going underwater if the RV depreciates quickly.

- Zero-down financing is available from some lenders but comes with higher rates and a greater risk of owing more than the vehicle is worth.

- Lenders also evaluate your debt-to-income ratio. A DTI under 36–43% is preferred, and RV lenders scrutinize overall financial health more carefully than standard auto lenders.

Pro Tip: Pull your credit report from AnnualCreditReport.com at least 60 days before applying. Dispute any errors and pay down revolving balances to improve your score before lenders see it. Even a 20-point improvement can move you into a better rate tier.

If your credit needs work, reviewing ATV financing for bad credit strategies can show you practical steps that apply equally to RV loan preparation.

What documents do you need to get an RV loan?

The application process for an RV loan follows a clear sequence. Being prepared with the right documents speeds up approval and reduces back-and-forth with lenders.

Applying for an RV loan requires detailed RV specs and financing amounts, including taxes, title, registration, and optional warranties. Lenders also need a full picture of your financial situation.

Here is the standard step-by-step process:

- Check your credit score and review your credit report for errors before applying anywhere.

- Gather your financial documents, including recent pay stubs, two years of tax returns, and a list of current debts and monthly obligations.

- Collect RV details, including the VIN, make, model, year, mileage, and purchase price.

- Apply for pre-approval with at least two or three lenders to compare offers. Many lenders pre-approve within 24–48 hours.

- Compare loan offers side by side, focusing on APR, total interest paid, loan term, and any prepayment penalties.

- Close the loan and finalize the purchase, confirming all fees are disclosed upfront.

| Document | Purpose | Typical Turnaround |

|---|---|---|

| Pay stubs (last 30 days) | Verify income | Immediate |

| Tax returns (2 years) | Confirm income stability | Immediate |

| RV VIN and specs | Confirm collateral value | Immediate |

| Debt statements | Calculate DTI ratio | Immediate |

| Pre-approval letter | Negotiate with dealer | 24–48 hours |

Having every document ready before you start the process cuts approval time significantly and signals to lenders that you are a prepared, low-risk borrower.

How to compare and negotiate RV loan offers

Comparing loan offers is where most buyers leave money on the table. The monthly payment number is the least useful figure to focus on. Total interest paid over the loan term is what actually determines cost.

Dealer financing often includes a 1–3% rate markup as a commission the dealer earns for arranging the loan. That markup is not disclosed as a line item. You only see it buried in the APR. On a $50,000 loan, a 2% markup can add $5,000 or more in total interest.

Key steps to protect yourself when comparing offers:

- Request out-the-door pricing from the dealer before discussing financing. This separates the vehicle cost from the loan cost.

- Shop multiple lenders within a short window. Multiple credit inquiries within 14–45 days are grouped as a single inquiry by credit bureaus, so your score takes minimal impact.

- Review prepayment policies carefully. Some lenders charge penalties if you pay off the loan early.

- Check for add-ons like extended warranties or GAP insurance rolled into the loan. These inflate the financed amount and total interest.

Pro Tip: Get pre-approved by a credit union or online lender before visiting any dealership. Walk in with a written offer in hand. Dealers will often match or beat an independent rate to keep the financing in-house, which gives you a better deal either way.

Understanding wholesale vehicle purchasing can also reduce the purchase price you need to finance, which directly lowers your loan amount and total interest.

What ownership costs should you budget beyond the loan payment?

The monthly loan payment is only one part of what an RV actually costs you. Buyers who focus only on the payment often find themselves financially stretched within the first year of ownership.

Total RV ownership costs, including insurance, storage, maintenance, fuel, and campsite fees, should stay under 10–15% of your take-home pay for financial comfort. That benchmark is a practical ceiling, not a suggestion.

Here is a realistic breakdown of costs to budget for:

- Insurance premiums: Class A motorhomes cost significantly more to insure than Class B or Class C vehicles. Rates vary by state, usage, and coverage level.

- Storage fees: If you cannot store the RV at home, monthly storage fees at a facility typically run $50–$200 per month depending on your region.

- Maintenance and repairs: Tires, roof seals, engine service, and appliance upkeep add up. Budget at least 1–2% of the vehicle’s value annually.

- Fuel costs: Larger motorhomes average 6–10 miles per gallon. A single weekend trip can cost $100–$300 in fuel alone.

- Campsite and park fees: Full-hookup sites at private campgrounds average $40–$80 per night.

Depreciation is the hidden cost most buyers underestimate. RVs lose value faster than passenger cars, which means if you finance 100% of the purchase price, you may owe more than the vehicle is worth within the first two years. A solid down payment and a shorter loan term are the best defenses against this.

Reviewing types of recreational vehicles before you commit to a purchase helps you match the vehicle class to your actual usage, which directly affects insurance, fuel, and maintenance costs.

Key takeaways

Securing affordable RV financing requires credit preparation, lender comparison, and full ownership cost budgeting before you sign any paperwork.

| Point | Details |

|---|---|

| Credit score drives your rate | A score of 740 or above qualifies for the best APRs; below 680 means higher costs. |

| Down payment protects equity | A 20% down payment lowers your rate and prevents owing more than the RV is worth. |

| Dealer markup adds real cost | Dealer financing often adds 1–3% to your rate; independent pre-approval is your best defense. |

| Shop lenders within 14–45 days | Multiple inquiries in that window count as one, so compare freely without credit damage. |

| Budget beyond the payment | Total ownership costs should stay under 10–15% of take-home pay to stay financially comfortable. |

What i have learned after years of watching buyers finance recreational vehicles

The biggest mistake I see buyers make is treating the monthly payment as the finish line. A dealer can stretch a loan to 20 years and make almost any RV look affordable on paper. The total interest paid on a $60,000 RV financed over 20 years at 8% is staggering. Most buyers never run that number before signing.

My honest advice: get pre-approved by a credit union before you set foot in a dealership. Navy Federal Credit Union and local credit unions consistently offer lower rates than dealer-arranged financing. Walking in with a written offer changes the entire dynamic of the negotiation. Dealers know you are serious and that you have done your homework.

I also think buyers underestimate how much the vehicle class affects long-term costs. A Class A motorhome is a completely different financial commitment than a travel trailer or a utility vehicle. If you are new to recreational vehicle ownership, starting with a smaller, less expensive vehicle and financing it conservatively is the smarter path. You learn what you actually use, what you actually need, and you avoid being locked into a 15-year loan on a vehicle that sits in storage nine months a year.

Credit preparation is not glamorous, but it is the highest-return activity you can do before applying. Sixty days of focused credit improvement, paying down balances and disputing errors, can save you more money than any negotiation tactic at the dealership.

— Gary

Browse recreational and utility vehicles at Importjunkies

Importjunkies carries a wide range of recreational and utility vehicles, from electric golf carts to gas-powered ATVs and UTVs, all available at wholesale pricing direct to the public. Whether you are financing your first off-road vehicle or adding to your fleet, the inventory is built for buyers who want real value without dealer markups. The 48V Electric Golf Cart Renegade Edition and the 400cc 4x4 UTV with Snow Plow are two popular options with clear pricing so you can calculate your financing needs before you apply. Browse the full catalog at Importjunkies and contact the customer service team for help matching a vehicle to your budget.

FAQ

What credit score do you need for an RV loan?

Most lenders require a minimum credit score of 680 for competitive RV loan rates, with 740 or above qualifying for the best available APRs. Borrowers below 680 can still get approved but will pay higher interest rates.

How long are typical RV loan terms?

RV loan terms typically range from 60 to 240 months, or 5 to 20 years, depending on the loan amount and lender. Longer terms reduce monthly payments but significantly increase total interest paid.

Is dealer financing a good option for RV loans?

Dealer financing is convenient but often includes a 1–3% rate markup as a dealer commission. Getting pre-approved independently through a credit union or online lender gives you a benchmark to negotiate against.

How much should you put down on an RV?

A down payment of 20% or more is the standard recommendation. It lowers your interest rate by 0.5–1.0%, reduces your monthly payment, and protects you from owing more than the RV is worth if it depreciates quickly.

Can you finance a used RV?

Yes, but lenders often restrict financing to RVs that are 10–15 years old or newer. Older vehicles may require specialty lenders or personal loan products, and rates are typically higher due to increased collateral risk.

Recommended

- Must-Have Recreational Vehicles 2026: Top Picks Guide – Saferwholesale || Import Junkies || Great Sports

- Why Purchase Wholesale Vehicles: Save More in 2026 – Saferwholesale || Import Junkies || Great Sports

- Small Business Vehicle Selection Guide for 2026 – Saferwholesale || Import Junkies || Great Sports

- ATV Financing for Bad Credit That Works – Saferwholesale || Import Junkies || Great Sports